Introduction: The Unseen Tax on Everything We Buy

There’s a hidden tax on nearly everything you buy. It’s not a government tax, but it’s just as pervasive and, in many ways, more insidious. Every time a customer swipes, taps, or clicks to pay, a complex, opaque system siphons off a percentage of that money before it ever reaches the merchant. This is the world of interchange fees.

In the United States alone, merchants paid over $126 billion in credit and debit card processing fees last year. Let that number sink in. That's more than the entire GDP of Puerto Rico. This isn't just a "cost of doing business"; it's a colossal wealth transfer from Main Street businesses and their customers to a handful of giant financial institutions and payment networks. It's a system that stifles the growth of small businesses, inflates prices for every consumer, and funnels capital away from innovation and into the pockets of entrenched intermediaries.

For any merchant, from a corner coffee shop to a global e-commerce giant, the core Job-to-be-Done (JTBD) is simple: "Obtain payment for goods and services instantly, securely, and with minimal value leakage to intermediaries."

For decades, we’ve been told that the 2-4% fee is an unavoidable price for convenience and security. But what if it’s not? What if the entire system is an elaborate, outdated construct that’s ripe for disruption? This article makes a bold claim: the tools to dismantle this fee structure finally exist. But the path forward isn't what you think. I'll first dissect the failure of the most-hyped solution—Real-Time Payments—and reveal why it's a dead end for retail. Then, I’ll will lay out a practical, two-tiered strategy using a technology you might have dismissed: stablecoins. This is the roadmap to finally achieving the job of payment, not as a source of revenue for banks, but as a solved, invisible piece of infrastructure for the entire economy.

Part 1: The Fortress of Fees: Why the Current System is So Hard to Change

To understand why this $126 billion problem persists, you have to see the system for what it is: a brilliant, self-reinforcing fortress. It's built on a foundation of complexity, protected by a moat of incentives, and defended by its most loyal soldiers: the consumers themselves.

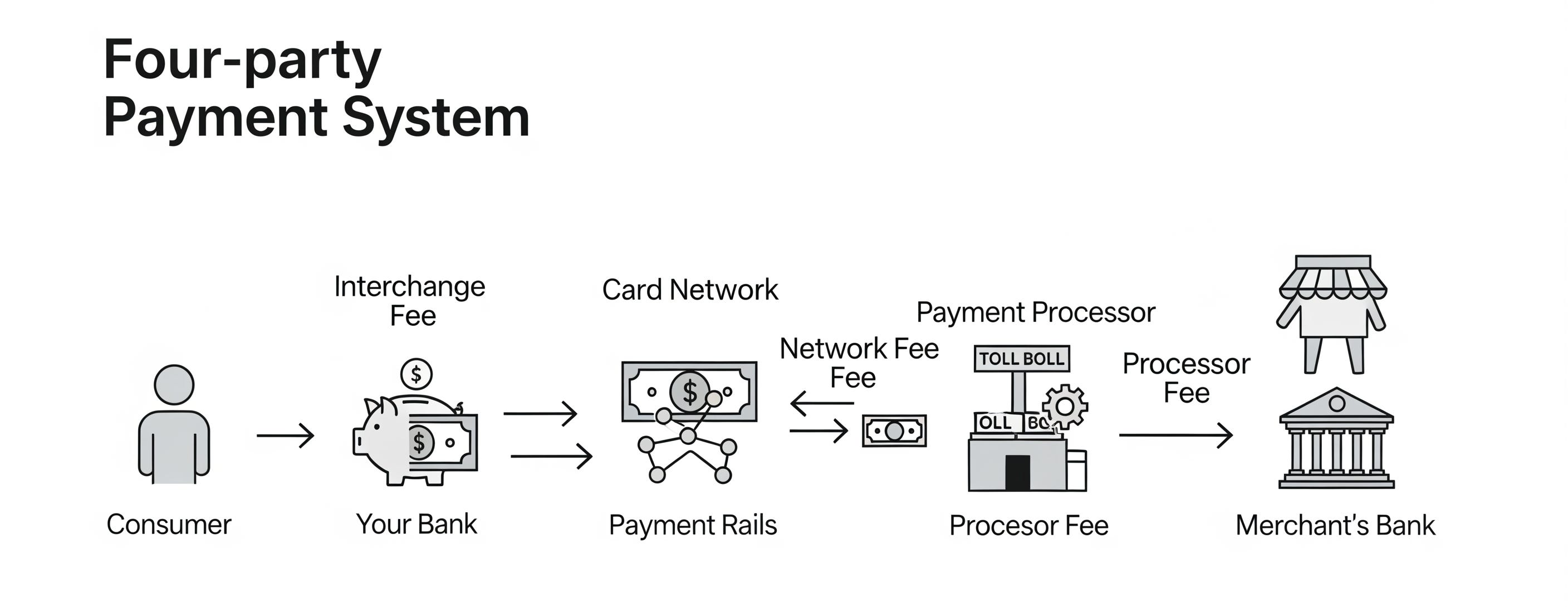

Imagine the payment system as a series of toll roads. When you buy something, the money doesn't go directly from your bank to the merchant. It travels on roads owned by Visa or Mastercard. Along the way, it passes through several tollbooths:

The Issuing Bank (Your Bank): The bank that issued your credit card takes the biggest cut. This is the "interchange fee."

The Acquiring Bank (The Merchant's Bank): This bank handles the transaction for the merchant and takes a smaller cut.

The Payment Processor: This is the company (like Square, Stripe, or Fiserv) that provides the hardware and software, and they take their own fee.

The Card Network (Visa/Mastercard): They own the highway and charge a network fee for using their rails.

This complexity isn't a bug; it's a feature. It obscures where the money is going, making it nearly impossible for a merchant to negotiate the single biggest part of the fee—the interchange—which is set by the card networks in a duopolistic fashion.

But the true genius of this fortress is its moat: consumer rewards.

Why do you use your Sapphire Reserve or your Platinum Amex? The points, the miles, the cashback. Banks present these rewards as a generous perk, a gift for your loyalty. This is a carefully crafted illusion. Banks aren't giving you free money; they are bribing you with the merchant's money, which is ultimately your money.

Here's how it works: Banks charge merchants high interchange fees. They then take a portion of that fee revenue and give it back to you, the cardholder, in the form of rewards. Merchants, forced to pay these high fees, have no choice but to bake those costs into the prices of their goods and services. So, the 2% cashback you feel so good about? You already paid for it through slightly higher prices on everything you buy. The system forces cash payers and debit users to subsidize the rewards of premium credit card holders.

This makes consumers—especially affluent ones—the system's staunchest defenders. You're not just a user; you're a stakeholder. And you'll fight to protect the "perks" you receive, making it incredibly difficult for any new system that doesn't offer a competing benefit to gain a foothold.

Part 2: The False Dawn: Why Real-Time Payments (RTP) Aren't the Answer for Retail

For the last few years, a new hope has been quietly building in the fintech world: Real-Time Payments (RTP). Networks like The Clearing House's RTP® and the Federal Reserve's FedNow® Service promised a new era of instant, direct bank-to-bank transfers. On the surface, they seem like the perfect solution.

These networks are real, they are live, and they are available to the vast majority of U.S. bank accounts. They can move money from one account to another, 24/7/365, for a literal fraction of a penny. The dream was that this would become the new payment rail for retail, completely bypassing the expensive card networks.

But it hasn't happened. And it won't. RTP, for all its technical prowess, is a false dawn for retail because it fundamentally fails to solve the complete job of a consumer transaction. It has three critical, unfixable flaws.

Flaw #1: The Irrevocability Problem & The Trust Deficit

This is the single biggest showstopper. RTP transactions are final. They are like digital cash. Once you send the money, it's gone. There is no built-in way to reverse it.

This is a catastrophic failure for consumer retail. The entire e-commerce and modern retail landscape is built upon a foundation of trust, and that trust is underwritten by one powerful mechanism: the chargeback. If you buy a product that never arrives, is a cheap counterfeit, or is clearly not as advertised, you can call your credit card company and get your money back. If your card number is stolen and used fraudulently, you are not liable. This consumer protection is the bedrock of confidence in digital payments.

RTP offers no equivalent. In an RTP world, if you pay for a product from a shady online store and they send you a box of rocks, you have no recourse through the payment system. The risk shifts entirely from the bank to the consumer. This is a trust deficit that cannot be overcome. No sane consumer would willingly give up this protection for the vast majority of their purchases.

Flaw #2: The "Push vs. Pull" User Experience Nightmare

The second flaw is more subtle but just as damning. It’s about the user experience (UX) at the point of sale.

Card Payments are a "PULL" transaction: You tap your card, and the merchant's system pulls the correct amount of money from your account. The interaction is passive, fast, and requires minimal effort from you.

RTP is a "PUSH" transaction: You, the customer, must actively push the funds to the merchant.

Now, visualize the real-world consequence of this. You're at a busy coffee shop, and your total is $5.87. With a card, you tap and go. In an RTP world, the flow would be something like this:

The barista tells you the total is $5.87.

You take out your phone and unlock it.

You open your specific banking app.

You navigate to the "Pay or Transfer" section.

You have to input the merchant's unique identifier (their phone number? an email? a cryptic code?).

You have to manually type in the exact amount: $5.87.

You hit send, authenticate, and wait.

The barista has to have a separate screen or system to verify they received your specific $5.87 payment, not the payment from the person behind you.

This is a UX disaster. It’s slow, cumbersome, and prone to error. In a world optimized for speed and convenience, it’s a giant leap backward.

Flaw #3: The Incentive Vacuum

Finally, even if you could magically solve the first two problems, you're left with the coldest reality of all: what's in it for the consumer?

Why would a customer voluntarily give up their 2% cashback, their airline miles, and their fraud protection to use a system that is clunkier and offers them nothing in return? They wouldn't. The merchant saves money, but the consumer gains nothing. In fact, they lose their valuable rewards. The value proposition is not just zero; it's negative.

RTP is a powerful technology that is genuinely transformative for other use cases like B2B payments, insurance payouts, and instant payroll. But for retail, it’s a solution to a problem that consumers don't have, while simultaneously ignoring the problems it creates for them. It’s a classic case of a technology looking for a problem, and it's a dead end for abolishing interchange fees.

Part 3: The Real Revolution: A Novel Strategy Using Stablecoins

If RTP is a false dawn, where do we turn? The answer lies in elevating the level of abstraction. The goal isn't just to find a cheaper way to send dollars through the old financial pipes. The goal is to create a new, parallel set of payment rails that are inherently cheaper, faster, and more efficient.

This is where stablecoins come in.

Before you roll your eyes, it's critical to separate speculative crypto assets like Bitcoin from utility-focused, asset-backed stablecoins. For our purposes, a stablecoin is simply a digital token that represents a one-to-one claim on a real dollar held in a regulated financial institution. Think of it as the digital equivalent of a casino chip. It’s a placeholder for the real money, making it incredibly easy to transfer and account for digitally. The most prominent examples are USDC (from Circle) and PYUSD (from PayPal).

Using stablecoins for payments isn't a theoretical fantasy. It’s happening right now, and it presents a two-tiered strategy to finally escape the fortress of fees.

Strategy 1: The On-Ramp Solution (Working Today)

Right now, any merchant can partner with a modern payment processor like Stripe, Sphere, or Coinbase Commerce to accept stablecoin payments. The process is remarkably simple and solves many of the problems RTP couldn't.

Here’s how a typical transaction works:

A customer is ready to pay online. Alongside "Pay with Card" and "PayPal," they see an option like "Pay with Crypto" or "Pay with Wallet."

They select this option and are prompted to pay with a stablecoin (like USDC) from their own digital wallet (e.g., Coinbase, Phantom, or a browser extension wallet).

The customer scans a QR code or connects their wallet and approves the transaction. The stablecoins move over a fast, cheap blockchain network (like Solana, Polygon, or an Ethereum Layer 2) and arrive in the merchant's account in seconds.

Here’s the magic: The merchant’s payment provider can be configured to instantly convert the stablecoin into U.S. dollars and deposit them into the merchant's regular bank account.

From the merchant's perspective, they never have to touch or hold a volatile crypto asset. They just receive dollars in their bank account, faster than an ACH transfer and for a fraction of the cost of a card transaction. The fee for this entire process can be around 1%, a massive saving compared to the typical 2.9% + $0.30 for online card payments. They have successfully bypassed the interchange system.

Strategy 2: The Novel Concept for a Fee-Free Future: The Merchant Settlement Alliance (MSA)

The on-ramp solution is a powerful tool for individual businesses, but the truly revolutionary step is to create a new, shared ecosystem. This is the novel strategy: a Merchant Settlement Alliance (MSA).

Imagine a consortium of the world's largest merchants—think Walmart, Amazon, Target, Shopify, and their peers—coming together to create and govern an open-source, standardized protocol for stablecoin payments. This wouldn't be a proprietary "Amazon Coin." It would be a neutral, shared infrastructure, like a digital version of the shipping container—a standard that everyone can use to make the entire ecosystem more efficient.

This alliance wouldn't just be a thought experiment; it's a strategic imperative that directly solves the core problems that killed RTP for retail:

Solving the Incentive Problem: The MSA's founding members currently pay tens of billions of dollars in interchange fees annually. By creating their own payment rail, they could redirect a portion of those massive savings to fund a rewards program that directly competes with premium credit cards. Imagine a universal 2% "Alliance Cashback" on all stablecoin purchases, instantly credited to your wallet and redeemable at any participating merchant. Suddenly, the consumer has a compelling reason to switch.

Solving the UX Problem: A standardized protocol is the key to a seamless user experience. It would allow Apple Pay, Google Pay, and other digital wallets to integrate this new payment method natively. The experience would become identical to what we have today: tap-to-pay with your phone or watch. But instead of the transaction routing through Visa, it routes through the MSA's stablecoin rails. The complexity is hidden, and the experience is fast and familiar.

Solving the Trust Problem: With billions in pooled resources, the MSA could establish its own robust consumer protection and dispute resolution system. They could fund an insurance pool to cover fraudulent transactions and create a clear, streamlined process for handling disputes over goods and services. They could replicate the function of chargebacks without the exorbitant overhead and snail's pace of the legacy banking system.

The end result of the MSA is an innovation that demonstrates the principle of achieving a better outcome with fewer visible features. The consumer experience is simplified to a single, rewarding payment method. The merchant experience is simplified to a single, ultra-low-cost system that settles funds instantly. The complexity of the four-party system is abstracted away and replaced by a more elegant, efficient, and equitable model.

Part 4: Deconstructing the Innovation: Creativity Triggers in Action

The concept of the Merchant Settlement Alliance doesn't emerge from a vacuum. It can be systematically derived by applying creativity triggers to the core problem. These triggers force us to look at the components of the system differently.

Here's how several triggers from the Creativity Trigger framework lead directly to this novel solution:

Part 5: The Roadmap and The Hurdles

Creating this new reality is a monumental task, but it's not impossible. The path forward will be led by a few key players and must overcome significant hurdles.

The First Movers:

Large Retailers: The catalyst must be one or two of the largest retailers on the planet. A company like Walmart or Amazon has the scale, resources, and transaction volume to single-handedly create a powerful gravitational pull for the ecosystem.

Fintech & Payment Processors: Companies like Stripe, Block, and PayPal are essential. They have the technical expertise and existing merchant relationships to build the user-facing apps, the on/off-ramps from fiat to stablecoins, and the seamless wallet integrations.

Stablecoin Issuers: Circle (USDC) is a key player, having already built the regulated, dollar-backed infrastructure that can serve as the settlement asset for the entire network.

The Hurdles:

Regulatory: This is the most significant challenge. Navigating the evolving landscape of digital asset regulation in the US and globally will require immense legal and lobbying efforts. However, by focusing on fully-backed stablecoins issued by regulated entities, the MSA can position itself as a compliant and transparent financial innovation.

Technical: Building a system that is secure, scalable to millions of transactions per second, and seamlessly interoperable across countless different merchants and wallets is a massive engineering challenge.

Adoption: The final, and perhaps largest, hurdle is changing deeply ingrained consumer behavior. Overcoming the inertia of the credit card habit will require a flawless user experience and a rewards program that is not just competitive, but demonstrably superior to what the banks offer.

Conclusion: A Choice, Not an Inevitability

The $126 billion-plus in annual interchange fees is not a law of physics. It is not an unavoidable cost. It is the legacy of an outdated, inefficient system that has been protected by inertia and misaligned incentives for far too long.

I've shown that the most talked-about solution, Real-Time Payments, is a dead end for retail—a technically sound system that is behaviorally and structurally wrong for the job.

The real path forward, a path that is both technologically viable and economically compelling, lies with elevating our thinking from simply moving dollars to truly settling value. A two-pronged strategy centered on stablecoins offers a way out. Individual merchants can act today to slash their fees using existing on-ramp solutions. And looking forward, a collaborative Merchant Settlement Alliance holds the revolutionary potential to build a new, parallel financial rail that is fairer, more efficient, and more innovative for everyone.

This future isn't guaranteed. It requires courage from corporate leaders, ingenuity from engineers, and a willingness from all of us to imagine a system where value flows freely, without the friction of unnecessary intermediaries. The question is no longer if merchants can escape the fortress of fees, but if they have the collective will to build the alternative.

I've laid out a strategic path for merchants to create their own payment network. What do you think is the single biggest non-technical hurdle to getting major, competing retailers to collaborate on a project like this? Share your thoughts in the comments.

Follow me on 𝕏: https://x.com/mikeboysen

If you'd like to see how I apply a higher level of abstraction to the front-end of innovation, please reach out. My availability is limited.

Mike Boysen - www.pjtbd.com

Why fail fast when you can succeed the first time?

📆 Book an appointment: https://pjtbd.com/book-mike

Join our community: https://pjtbd.com/join

Share this post