Table of Contents

Elevating the Abstraction: From Complex Policies to Simple Outcomes

Pillar 1: Proactive Insurance - Preventing the Claim in the First Place

Pillar 2: Parametric Insurance - Automated Payouts for Predetermined Events

Pillar 3: Embedded and Invisible Insurance - Protection at the Point of Need

Introduction: The Unseen Risk in Your Insurance Policy

You pay your premiums diligently every month. You have a folder—digital or physical—filled with policy documents for your home, your car, your health, your business. You feel responsible. You feel protected. But are you?

Consider the story of a small business owner who, after a flood damaged their inventory, discovered their "comprehensive" policy didn't cover that specific type of water damage. Or the family who faced a massive medical bill, only to learn the specialized procedure they needed wasn't included in their network. These stories aren't exceptions; they are the logical outcomes of a broken system.

The fundamental "Job to be Done" of insurance is simple: to achieve financial security and peace of mind in the face of uncertainty. Yet, the industry designed to perform this job has become a labyrinth of legalese, exclusions, and processes that place the burden of proof squarely on you, the customer, precisely when you are most vulnerable.

The current insurance model fails at its core job because it is built on a foundation of complexity and reaction. It waits for the disaster to strike. A new, more effective model is emerging, one that flips the script entirely. The future of insurance is proactive, parametric, and embedded.

Elevating the Abstraction: From Complex Policies to Simple Outcomes

To understand this shift, you need to grasp one key idea: elevating the level of abstraction.

In simple terms, it means moving from dealing with messy, complicated details to focusing on a simple, desired outcome.

Today's Reality (Low Abstraction): You are forced into the weeds. You juggle multiple policies from different providers—home, auto, life, health. Each is a dense document you're expected to read and understand. The "job" has become managing and deciphering complex instruments, not achieving security. The work is on you.

The Future (High Abstraction): You are removed from the weeds. Imagine a single, integrated view of your risk posture. You don't buy "a policy"; you secure a guaranteed outcome. You are protected from financial loss, period. The immense complexity of risk calculation, prevention, and payout is handled by technology and innovative models working seamlessly in the background. The experience is simple, intuitive, and focused on the outcome.

[Image: A diagram illustrating the shift from a fragmented, messy pile of insurance documents on one side to a clean, single dashboard on a tablet showing "Overall Financial Security: Protected" on the other.]

This isn't a fantasy. It's a new paradigm built on three powerful pillars that are already changing the industry.

Pillar 1: Proactive Insurance - Preventing the Claim in the First Place

The most profound shift in the insurance model is moving from a reactive "break-fix" mentality to a proactive, preventative one. The best claim is the one that never has to be filed.

How it works today (for the few): We see glimpses of this in usage-based auto insurance (UBI) like Progressive's Snapshot, which rewards safe driving with lower premiums. In health insurance, programs like John Hancock's Vitality use data from wearables to offer rewards for healthy habits like regular exercise. These are the first steps.

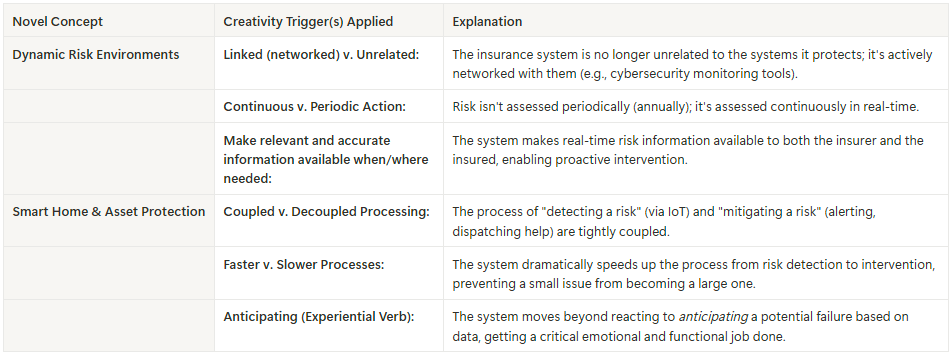

Novel Concepts (getting the job done better):

Dynamic Risk Environments: Think of a business's cybersecurity insurance. Instead of an annual policy based on a static questionnaire, the insurance is directly integrated with the company's real-time security monitoring tools. The insurer acts as a partner, proactively flagging vulnerabilities. As the company's security posture improves, its premiums automatically decrease. The job of "maintaining cybersecurity" and "insuring against breaches" become one and the same.

Smart Home & Asset Protection: For a homeowner, this means an insurance service that is connected to their IoT devices. It detects the small water leak from a faulty pipe and alerts you—or even dispatches a plumber—before it floods your basement. It detects unusual heat signatures and warns of a potential fire hazard before the smoke alarm goes off. The insurance doesn't just pay for the catastrophic damage; it actively works to prevent it.

Creativity Trigger Reference Table: Proactive Insurance

Pillar 2: Parametric Insurance - Automated Payouts for Predetermined Events

One of the most painful parts of insurance is the claims process. It's slow, adversarial, and uncertain. Parametric insurance eliminates this pain by making claims objective and automatic.

Instead of paying based on a subjective assessment of your loss, a parametric policy pays a predetermined amount when a specific, measurable event occurs—a parameter is met.

How it works today: This is already used in industries where risk is easily quantifiable. A farmer might buy a policy that automatically pays out if rainfall in their region is below a certain level for a set number of weeks. A resort might have a policy that pays if a hurricane of a specific category makes landfall nearby. There's no adjuster, no debate. The parameter was met, the payout is triggered.

Novel Concepts (getting the job done better):

Personalized Parametric Policies: Imagine a health insurance supplement that is parametric. If you receive a diagnosis for a specific condition (e.g., Stage 2 cancer), the policy automatically pays a lump sum of $50,000 to your account within 24 hours. This provides immediate liquidity for treatment, travel, or lost income, getting the job of "reducing financial stress during a health crisis" done instantly.

Supply Chain Insurance: For a manufacturer, their greatest risk might be a key supplier going offline. A parametric policy could be written to trigger an automatic payout if that supplier's factory is non-operational for more than three days due to a verifiable, public event like a regional power outage or natural disaster. This provides immediate working capital to expedite shipping from an alternative supplier.

Creativity Trigger Reference Table: Parametric Insurance

Pillar 3: Embedded and Invisible Insurance - Protection at the Point of Need

The final pillar removes the friction of buying insurance altogether by embedding it seamlessly into other products and services. If the goal is to be protected, why should you have to take a separate, deliberate step to acquire that protection?

How it works today: You already see this in its simplest forms. When you book a flight, you're offered travel insurance with a single click. When you buy a new appliance, you're offered an extended warranty at the point of sale. These are convenient, but they are still visible, optional add-ons.

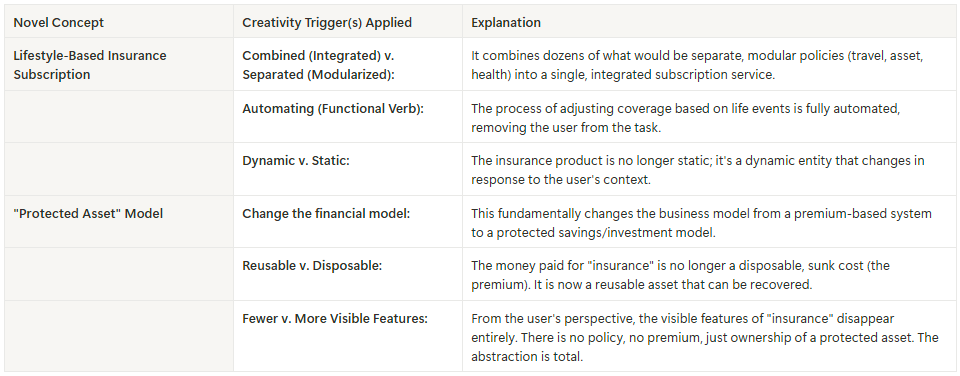

Novel Concepts (getting the job done better):

Lifestyle-Based Insurance Subscription: Imagine a single insurance subscription that dynamically adjusts your coverage based on your life. With your permission, it sees you've booked a ski trip to Colorado and automatically enhances your health and accident coverage for that week. It sees you've just bought a new e-bike and automatically adds it to your asset protection. You don't do anything; you just live your life, knowing your protection is adapting with you.

The "Protected Asset" Model: This is the ultimate elevation of abstraction. When you buy a high-value asset like a car or expensive camera, a percentage of the purchase price is automatically placed into a protected, ring-fenced "insurance fund" tied to that specific item. This fund is your money, earning interest. If you need to make a claim, the funds are instantly available. If you go claim-free for the life of the asset, you get the entire fund—plus its earnings—back when you sell it. This transforms insurance from a sunk cost into a form of savings.

Creativity Trigger Reference Table: Embedded and Invisible Insurance

Conclusion: The Future is About Outcomes, Not Exclusions

The current insurance paradigm forces you to be an expert in risk. The future allows you to be an expert in your own life, with the confidence that your security is being handled.

By shifting the focus to proactive prevention, enabling parametric speed, and creating embedded experiences, the insurance industry can finally move beyond the fine print. It can stop selling complex, confusing products and start delivering on the one, simple, vital job it was always meant to do: providing real peace of mind.

The revolution isn't coming; it's here. And it's built on a simple premise: the goal is the outcome, not the policy.

What is the biggest frustration you have with your current insurance? What "job" do you wish your insurance would do for you that it currently doesn't? Leave a comment below.

Follow me on 𝕏: https://x.com/mikeboysen

If you'd like to see how I apply a higher level of abstraction to the front-end of innovation, please reach out. My availability is limited.

Mike Boysen - www.pjtbd.com

Why fail fast when you can succeed the first time?

📆 Book an appointment: https://pjtbd.com/book-mike

Join our community: https://pjtbd.com/join

Share this post